Social Security beneficiaries will see a big jump in benefits in 2023. Yippee! But the increased income could trigger higher taxes.

An 8.7% cost of living adjustment (COLA) for 2023 to seniors claiming Social Security is the highest in 40 years. But although the extra income is welcomed by older adults caught in the vise of rising prices due to inflation, it could mean higher taxes and premiums. Strategic tax planning will be necessary for many retirees to avoid paying Uncle Sam more for benefits.

The large COLA is “great” for seniors, according to Brian Vosberg, a certified financial planner and president of Vosberg Wealth in Glendora, California. But there are hidden pitfalls to the increase for retirees. “While they’re excited to see the increase coming, they’re not really envisioning what the impact can be from a tax standpoint,” he says.

One important aspect of these increases is that the cutoff points are cliffs, rather than glide paths. If you are $1 over the limit, you will pay the increase. That’s why it’s so important to pay strict attention to the specific dollar amounts.

Social Security Taxes

Take Social Security itself. Taxes on benefits are based on a combined income formula that combines your adjusted gross income with nontaxable interest and half of your Social Security benefits. Your interest next year could be higher since rates have gone up, and added to higher benefits you may go over the tax threshold. It starts at just $25,000 for individuals and $32,000 for married couples.

Single filers with from $25,000 to $34,000 in combined income owe tax on up to half of their benefits. The threshold goes up to between $32,000 and $44,000 for married earners. Above those levels, up to 85% of Social Security may be taxed.

Taxes on benefits were initiated in 1983 when a mere 8% of families made enough income to owe them. But because the income levels have never been adjusted, approximately 56% of families paid taxes on benefits in 2021, according to the Center for Retirement Research.

Medicare Part B Premiums

Starting in 2007, Part B Medicare premiums are based on income. These levels affect higher earners, or about 7% of beneficiaries. Premiums for full Part B coverage in 2023 are shown in the following government-provided table.

Source: https://www.cms.gov/newsroom/fact-sheets/2023-medicare-parts-b-premiums-and-deductibles-2023-medicare-part-d-income-related-monthly

Medicare Part D Premiums

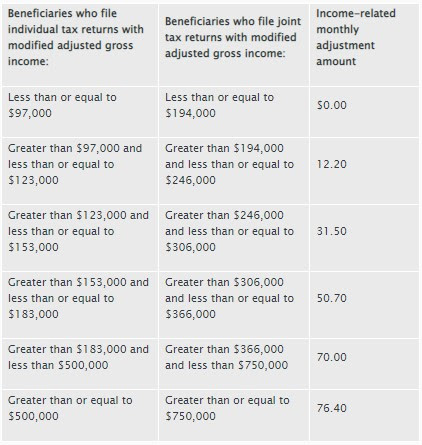

If your income puts you in a category for higher payments on your Part B premiums, you will also owe more for Part D coverage. Instituted in 2011, premium payments bump up for individual filers with an AGI higher than $97,000 and married couples whose AGI tops $194,000. Check out the government-provided chart below for specifics for both individuals and married couples filing jointly.

Source: https://www.cms.gov/newsroom/fact-sheets/2023-medicare-parts-b-premiums-and-deductibles-2023-medicare-part-d-income-related-monthly

Low-Income Benefits May Be Taken Away

You may think you’ve dodged a bullet if you are in a low income bracket, but you could be mistaken. Seniors receiving government assistance for benefits such as Medicare Extra Help, Medicaid, food stamps (SNAP), and rental help could be eligible for less or no aid if their income crosses certain thresholds.

The Centers for Medicare and Medicaid Services have eligibility requirements for Medicare Extra Help. Medicaid eligibility varies by state, so check your state for cutoffs. Visit the website for the Center on Budget and Policy Priorities to check eligibility for SNAP. Find eligibility limits for Section 8 housing here.

How to Avoid Higher Taxes and Premiums

The bottom line is that a professional tax planner or tax-focused financial planner may be essential for most retirees in 2023, even if you haven’t used one before. They can run the numbers and determine if you need to take a bit less out of your taxable account, and a bit more out of a Roth, or other workarounds.

But don’t wait to visit until April 15. The time to see a professional advisor is now when you can edit withdrawals for next year. Plan ahead so you can keep more of your Social Security increase to fight inflation.

Sources:

Blog posting provided by Society of Certified Senior Advisors